Adjustments

Medical Savings Account (Form 8853)

The Medical Savings Account Form in the tax program must be entered manually. Distributions from a Medical Savings Account are reported to recipients on Form 1099-MSA.

Educator Expenses

Teachers and other educators can deduct as much as $250 that they spent to purchase classroom supplies.

Expenses for Reservists and Performing Artists

National Guard and reserve members may qualify for special consideration. Those who travel over 100 miles from home to perform services as an armed forces reservist get to claim related business expenses on Line 24 of Form 1040 Schedule 1 after completing Form 2106.

Performing artists can deduct certain qualified expenses as well.

Health Savings Account (Form 8889)

If contributions (other than employer contributions) were made to the taxpayer’s health savings account, the taxpayer may be able to take this deduction.

Moving Expenses (Form 3903)

NOTE: The deduction for moving expenses have been eliminated until 2025, except for those who are in the armed forces.

This option in the Adjustments Menu allows the preparer to enter any Moving Expenses that the taxpayer may have if he or she is a member of the Armed Forces and moved due to a change of station. Form 3903 is used to calculate moving expenses to a new principal place of work within the United States or outside of the United States.

Contributions to SEP, SIMPLE and Qualified Plans

To qualify for this adjustment, the taxpayer must have self-employment income. Self-employment income consists of net profits from a Schedule C or Schedule F, or guaranteed payments from a partnership.

Additionally, the taxpayer must set up and fund a qualified retirement plan, such as a SEP-IRA, SIMPLE -IRA, or Keogh-type pension plan.

"SEP, SIMPLE, and qualified plans offer you and your employees a tax-favored way to save for retirement. You can deduct contributions you make to the plan for your employees. If you are a sole proprietor, you can deduct contributions you make to the plan for yourself. You can also deduct trustees' fees if contributions to the plan do not cover them. Earnings on the contributions are generally tax free until you or your employees receive distributions from the plan." (IRS Publication 560)

Self-Employed Health Insurance

Selecting this menu option allows the preparer to enter the taxpayer’s information for the Self-Employed Health Insurance Deduction Worksheet.

Penalty on Early Withdrawal

This is the penalty the taxpayer pays for withdrawing money from a savings plan, such as a certificate of deposit (CD), before its maturity date. For instance, if the taxpayer has a 2-year CD, but he or she withdraws the money after only one year, the bank may charge a penalty. Report the interest income in full, but preparers are allowed to take an adjustment to the taxpayer's gross income for the penalty.

Alimony Paid

NOTE: Under the new tax law, Alimony based on a divorce agreement that was modified or executed after 2018 can no longer be counted as income or as a deduction.

This is money paid to a spouse or former spouse because of a written separation agreement or a court order in a separate maintenance agreement or divorce decree. Alimony and separate maintenance payments are treated as follows on the next page:

- Taxable income to the receiver, and

- Deductible before adjusted gross income for the payer.

IRA Deduction (Not Roth IRA)

The taxpayer may present Form 5498-IRA Contribution Information.

Form 5498 - Box 1 – IRA Contributions – is for reporting contributions (deductible and nondeductible) to a Classic Individual Retirement Annuity (IRA) for the tax-reporting year. Use this menu option to enter these amounts as an adjustment to income.

Nondeductible IRAs (Form 8606)

This menu option is the entry point for Form 8606, which covers:

- Nondeductible Contributions to IRAs.

- Traditional IRA Distributions Received During the Tax Year.

- Net Amount of Traditional IRAs Converted to Roth IRAs.

- Distributions from Roth IRAs; and Distributions from Educational IRAs.

For detailed questions concerning Form 8606, see IRS Publication 590 – Individual Retirement Arrangements.

Student Loan Interest Deduction

The deduction is claimed as an adjustment to income, so the taxpayer does not need to itemize deductions on Schedule A.

A qualified student loan is a loan the taxpayer took out to pay qualified expenses. The expenses must have been:

- For the taxpayer, spouse, or a person who was the taxpayer’s dependent when the loan was taken out,

- Paid or incurred within a reasonable time before or after the taxpayer took out the loan, and

- For education furnished during a period when the recipient was an eligible student.

Qualified higher education expenses are the costs of attending an eligible educational institution, including graduate school. These costs include:

- Tuition

- Fees

- Books

- Equipment, and

- Other necessary expenses, such as transportation. (See IRS Publication 17 for additional information.)

Tuition and Fees Deduction (Form 8917)

The Tuition and Fees Deduction has been eliminated starting in 2018.

Domestic Production Activities Deduction (Form 8903)

The Domestic Production Activities Deduction has been repealed and eliminated for all taxpayer and entities starting in 2019.

The Other Adjustments Menu will offer several “Other Adjustment” menu entries for adjustments to income in addition to those previously described.

Other Adjustments

Jury Duty Pay – If a client served jury duty and their pay was included by their employer as normal W-2 wages, this adjustment will reduce their taxable income by the amount earned.

Credits Menu

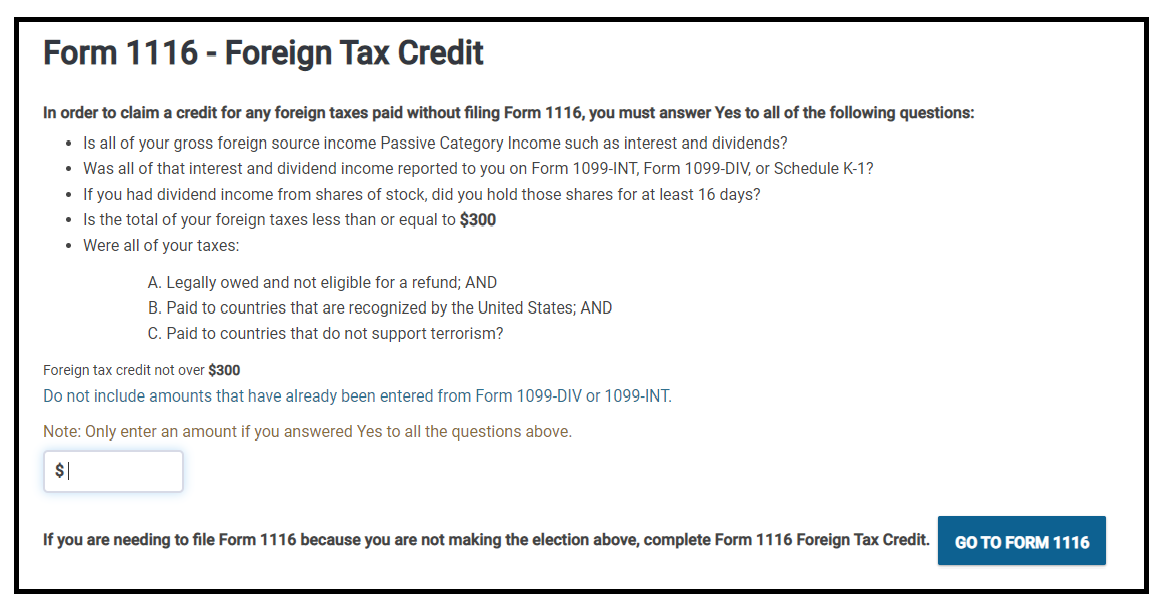

Foreign Tax Credit – Form 1116

Generally, a taxpayer’s Foreign Tax Credit will not exceed $300 ($600 if married filing joint), so in most cases preparers will enter the credit amount in the input box labeled “Foreign tax credit not over $300” in this menu.

The taxpayer can claim a credit for foreign income taxes, or taxes imposed by possessions of the U.S., that were paid or accrued during the tax year. For example, the taxpayer might have become liable for foreign taxes on profits from overseas operations or investments. The taxpayer can elect to deduct these taxes instead of taking the credit, if he or she prefers, although claiming the credit will generally provide a greater benefit. The credit is claimed on Form 1116, Foreign Tax Credit, which is accessed by clicking the “Go to Form 1116” button in the “Form 1116- Foreign Tax Credit” menu.

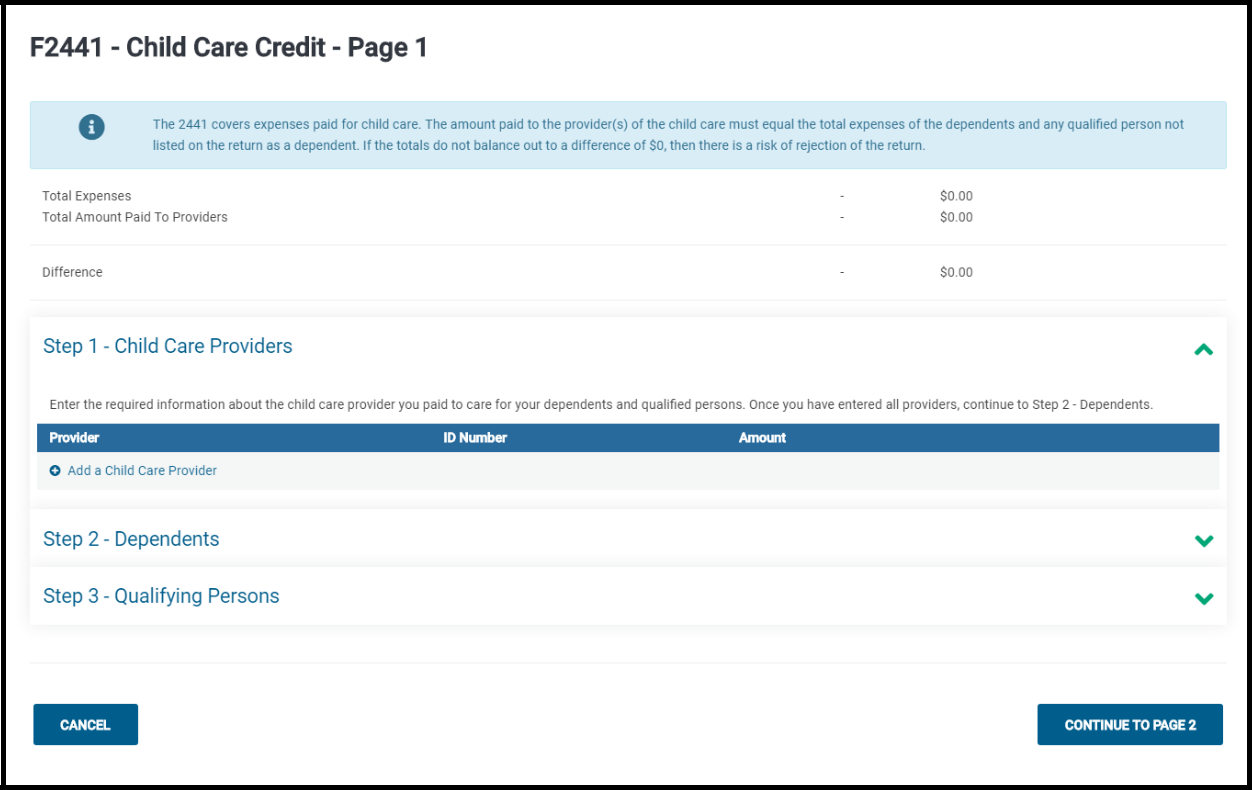

Child Care Credit Form 2441

To claim the credit for child and dependent care expenses, fill out Parts I and II of IRS Form 2441,

Child and Dependent Care Expenses.

This form requires the taxpayer to provide identification information for both the care provider(s) and the qualifying children or disabled persons. The form helps to compute the credit by comparing allowable expenses with the client's wages and other earnings (and those of the spouse, if married). The credit amount as shown on Line 11 of the 2441 is carried to Line 12a of the Form 1040, where it will be directly subtracted from the tax owed.

In the Form 2441 Menu, begin by entering the Amount Paid to Child Care Providers. For the return to be accepted electronically, this information must be filled out correctly. The tax return cannot be filed electronically without a valid Employer Identification Number or Social Security Number for the Daycare Provider.

How to fill out the Taxpayer's Earned Income, or the Spouse's Earned Income, on Form 2441, if one is a full-time student or disabled: When preparing a joint return where either the taxpayer or spouse was a full-time student or disabled, the Earned Income to be placed in the program for the non-working spouse is $250 per month ($500 per month if more than one qualifying person was cared for during the year). If the spouse also worked during the month, use the higher of $250 (or $500) or his or her actual earned income for that month. For example, if the taxpayer's wife is attending college full-time, and the couple has one child in daycare, enter $3000 in the Form 2441 menu.

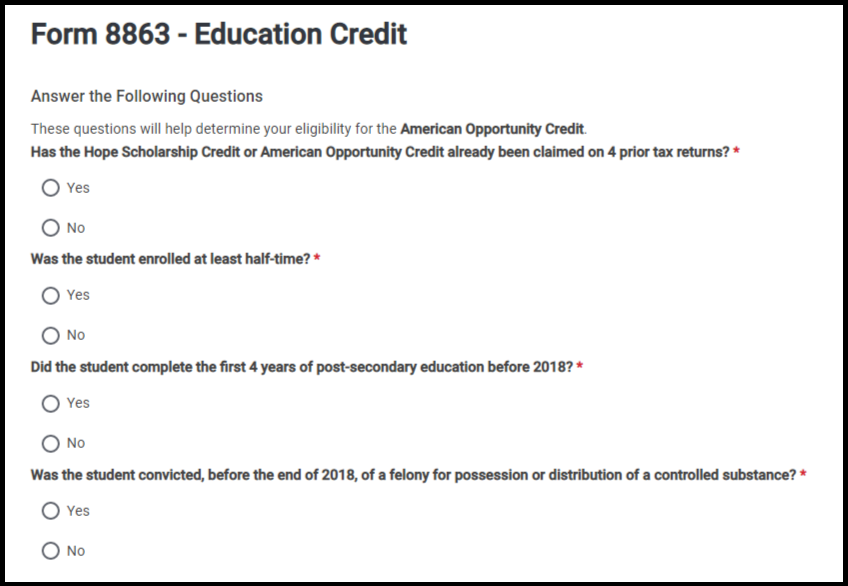

Education Credits—Form 8863 (Form 1098-T)

American Opportunity Tax Credit: 40% of this tax credit is refundable for undergraduate college education expenses; the rest is nonrefundable. This credit provides up to $2,500 in tax credits for adjusted qualifying educational expenses. The student must be enrolled at least half time for at least one academic period beginning during the tax year (or the first 3 months of the following year if the qualified expenses were paid in the tax year). The amount of credit is gradually reduced (phased out) if the taxpayer’s MAGI is between $90,000 if single, HOH, or qualifying widow(er) and $180,000 if filing a joint return). There is no credit if the MAGI is $90,000 or more ($180,000 or more if filing a joint return).

Lifetime Learning Credit: Students are not required to be enrolled at least half-time in one of the first two years of postsecondary education. The credit is available for all years of postsecondary education and for courses to acquire or improve job skills. The maximum lifetime learning credit on a return for any single year is up to $2,000, regardless of the number of students for whom the taxpayer paid qualified education expenses. The amount of credit for a given tax year is gradually reduced (phased out) if the taxpayer’s MAGI is $64,000 if single, HOH, qualified widow(er) and $134,000 if filing a joint return. A taxpayer cannot claim a credit if their MAGI is $64,000 or more ($134,000 or more if filing a joint return). Taxpayers cannot claim the lifetime learning credit for any student if they claim the American opportunity credit for that student for the same tax year. See Form 8863 Instructions for more information.

Tuition and Fees Deductions: This adjustment has been eliminated starting in 2018.

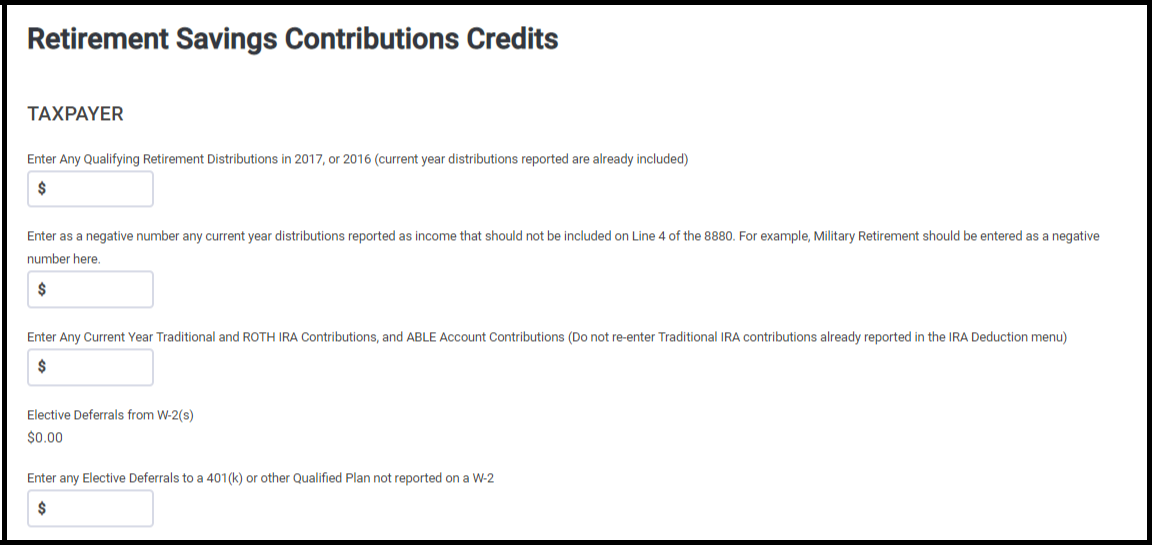

Retirement Savings Credit

If the taxpayer made eligible contributions to an employer-sponsored retirement plan or to an individual retirement arrangement, they may be eligible for a tax credit, depending on their age and income.

Income limits: The Savers Credit, formally known as the Retirement Savings Contributions Credit, applies to individuals with a filing status and the current tax year income not more than:

Single, married filing separately, or qualifying widow(er), with income up to $32,000

Head of Household with income up to $48,000

Married Filing Jointly, with incomes up to $64,000

Eligibility requirements: To be eligible for the credit the taxpayer must be at least 18 years of age, cannot have been a full-time student during the calendar year and cannot be claimed as a dependent on another person’s return.

Credit amount: If the taxpayer made eligible contributions to a qualified IRA, 401(k) and certain other retirement plans, they may be able to take a credit of up to $1,000 ($2,000 if filing jointly). The credit is a percentage of the qualifying contribution amount, with the highest rate for taxpayers with the least income.

Distributions: When figuring this credit, the preparer must generally subtract distributions the taxpayer received from their retirement plans from the contributions that they made. This rule applies to distributions received in the two years before the year the credit is claimed, the year the credit is claimed, and the period after the end of the credit year but before the due date - including extensions - for filing the return for the credit year.

Other tax benefits: The Retirement Savings Contributions Credit is in addition to other tax benefits the taxpayer may receive for retirement contributions. For example, most workers at these income levels may deduct all or part of their contributions to a traditional IRA. Contributions to a regular 401(k) plan are not subject to income tax until withdrawn from the plan.

Forms to use: To claim the credit use Form 8880, Credit for Qualified Retirement Savings Contributions.

The preparer may be able to take this credit if the taxpayer, or their spouse if filing jointly, made:

- Contributions (other than rollover contributions) to a traditional or Roth IRA,

- Elective deferrals to a 401(k) or 403(b) plan (including designated Roth contributions) or to a governmental 457, SEP, or SIMPLE plan,

- Voluntary employee contributions to a qualified retirement plan (including the federal Thrift Savings Plan), or

- Contributions to a 501(c)(18)(D) plan.

The taxpayer is not eligible to take the Retirement Savings Credit if any of the following applies:

- AGI exceeds the limit listed in the Form 8880 instructions.

- The person(s) who made the contributions or elective deferrals was

- Born after a date listed in the instructions for the form.

- Is a student (see below), or

- Is being claimed as a dependent on someone else's return for the same tax year.

Student: The taxpayer (or spouse if MFJ) is considered a "student" if, during any part of 5 calendar months during the tax year they either:

- Were enrolled as a full-time student at a school, or

- Took a full-time, on-farm training course given by a school or a state, county, or local government agency.

A "school" includes technical, trade, and mechanical schools. It does not include on-the-job training courses, correspondence schools, or schools offering courses only through the Internet.

Residential Energy Credit

The taxpayer may be eligible to take this credit if they made qualified energy saving improvements to their home located in the United States in the current tax year.

“For credit purposes, costs are treated as being paid when the original installation of the item is completed, or in the case of costs connected with the construction or reconstruction of the home, when the original use of the constructed or reconstructed home begins. If less than 80% of the use of an item is for nonbusiness purposes, only that portion of the costs that are allocable to the nonbusiness use can be used to determine the credit.” (IRS Form 5695 Instructions)

Home:

A home is where the taxpayer lived in the current tax year and may include things such as a house, houseboat, mobile home, cooperative apartment, etc. For a completed list of acceptable homes, please reference the IRS Instructions for Form 5695.

Main home: The main home is typically the residence where the taxpayer lived most of the time. Some exceptions, such as absence from education or illness will not change the main home.

Adoption Credit – Form 8839

You will use Form 8839 to determine if the taxpayer may qualify for an adoption credit and income exclusion if they have qualified adoption expenses. These expenses include adoption fees, attorney fees, and court costs. For an entire list of qualified expenses please refer to the IRS Form 8839 Instructions. Depending on the situation, the taxpayer may qualify for both the Adoption Credit and the income exclusion.

If the taxpayer is married, he or she must file a joint return with their spouse to claim either the qualified adoption expenses or the exclusion for employer-reimbursed adoption expenses, unless (1) they are legally separated, or (2) they have lived apart from for the last six months of the year and the home has been the child's home for more than half the year, and the taxpayer paid more than half the cost of keeping up the home for the year.

DC First-Time Homebuyer Credit – Form 8859

The taxpayer may be eligible to claim this credit if they purchased a main home during the tax year in the District of Columbia and the taxpayer (and spouse if married) did not own any other main home in the District of Columbia during the 1-year period ending on the date of purchase.

Mortgage Interest Credit - Form 8396

The taxpayer may be able to claim the credit only if they were issued a qualified Mortgage Credit Certificate (MCC) by a state or local governmental unit or agency under a qualified mortgage credit certificate program. Then the taxpayer can claim a tax credit based on the amount of interest they paid.

Earned Income Credit

If the Taxpayer qualifies for the Earned Income Credit, the tax program will automatically bring up the Form 8867-EIC Checklist Menu as you navigate to the E-File page.

If the taxpayer does not qualify to claim the Earned Income Credit and you access the EIC menu, you will be prompted to select Continue. You will be provided with a list of reasons why the Earned Income Credit is not being calculated on the Summary Page.

Information to Claim EIC After Disallowance

If the taxpayer was denied EIC for any year after 1996 or it was reduced for any reason other than a math or clerical error, you must attach a completed Form 8862 to their next tax return to claim the EIC. The taxpayer must also qualify to claim the EIC by meeting all the rules described in this IRS Publication 596.

There are three parts to Form 8862. The first part applies to everyone using the form and consists of three questions that basically establish that you should be filling out the form. The second part is to be filled out for taxpayers who are claiming a qualifying child. The third part is to be filled out for taxpayers who are not claiming a qualifying child.

EIC Information for Clergy

If you are preparing a tax return for a member of the clergy, and any amount of their clergy income should not be included in the calculation of the earned income calculation, enter the dollar amount to exclude in the space provided.

Not Eligible for EIC

If a taxpayer has been informed by the IRS that they are not eligible to claim the Earned Income Tax Credit this year, or if they simply want to opt out, place a check mark in the box next to this statement. Next, place a checkmark in the box stating that you understand that by checking the first box, EIC will not be calculated on this return.

Credit for the Elderly or Disabled

A tax credit is available to certain low-income individuals based on filing status, age, and income. If the taxpayer is married filing a joint return, it is also based on the spouse's age and income. The taxpayer may be eligible able to take this credit if either of the following applies:

- They were age 65 or older at the end of the current tax year, or

- They were under age 65 at the end of the current tax year and they meet all the following:

- They were permanently and totally disabled on the date that they retired. If they retired before 1977, they must have been permanently and totally disabled on January 1, 1976, or January 1, 1977.

- They received taxable disability income for the current tax year.

On January 1 of the current tax year they had not reached mandatory retirement age (the age when their employer's retirement program would have required them to retire).

Alternative Motor Vehicle Credit (Hybrid Cars) – Form 8910

Use this form to figure the credit for alternative motor vehicles placed in service during the tax year. The credit attributable to depreciable property (vehicles used for business or investment purposes) is treated as a general business credit. Any credit not attributable to depreciable property is treated as a personal credit.

NOTE: The alternative motor vehicle credit expired for vehicles purchased after 2017. Do not claim a credit for these vehicles on Form 8910 unless the credit is extended.

Qualified Electric Motor Vehicle Credit – Form 8936

Use this form to figure the credit for qualified plug-in electric drive motor vehicles placed in service during the tax year.

NOTE: Vehicles purchased after 2017 no longer qualify for this credit.

Small Employer Health Insurance Premiums – Form 8941

Eligible small employers may qualify for this credit if they paid health insurance premiums for their employers during tax years after 2009. The maximum credit is a percentage of premiums that the employer paid during the tax year for certain health insurance coverage the employer provided to certain employees. The credit may be reduced by limitations based on the employer’s full-time equivalent employees, average annual wages, state average premiums, and state premium subsidies and tax credits.

Credit for Federal Tax Paid on Fuels - Form 4136

Use this form to claim:

- A credit for certain nontaxable uses (or sales) of fuel during your income tax year,

- The alternative fuel credit, and

- A credit for blending a diesel-water fuel emulsion.

The use of fuels listed on the image shown:

Other Taxes

The Other Taxes portion of the Federal Section is used to enter any other tax types for which the taxpayer may be liable. Select the Begin button next to any other tax item to enter in data applicable to the taxpayer.

Self-Employment Tax - Schedule SE

If the taxpayer's total business income (from all Schedule C’s combined and from any partnership or S-corporation self-employment income) equals $400 or more, the tax program will automatically generate a Federal Schedule SE.

If the taxpayer is filing jointly and the spouse also files one or more Schedule C’s, each spouse must count his or her own income separately.

Alternative Minimum Tax - Form 6251

“Use Form 6251 to figure the amount, if any, of your alternative minimum tax (AMT). The AMT is a separate tax that is imposed in addition to your regular tax. It applies to taxpayers who have certain types of income that receive favorable treatment, or who qualify for certain deductions, under the tax law. These tax benefits can significantly reduce the regular tax of some taxpayers with higher economic incomes. The AMT sets a limit on the amount these benefits can be used to reduce tax.” (IRS Form 6251 Instructions)

A taxpayer is required to file the Form 6251 if any of the following apply:

- Line 7 on Form 6251 is greater than Line 10

- Any general business credit can be claimed

- Line 6 of Form 3800 OR Line 25 of Form 3800 is more than zero

- The qualified electric vehicle credit (Form 8834) was claimed

- The prior year minimum tax credit (Form 8801) was claimed

- The total of Form 6251 Lines 2c - 3 are negative

- If Line 7 would be more than Line 10 on the 6251 if Lines 2c - 3 were not taken into account

If the any of the about apply to the taxpayer’s return and the taxpayer's adjusted gross income exceeds the exemption amounts, the software will compute AMT liability on IRS Form 6251, Alternative Minimum Tax - Individuals, to determine whether the taxpayer must pay any AMT.

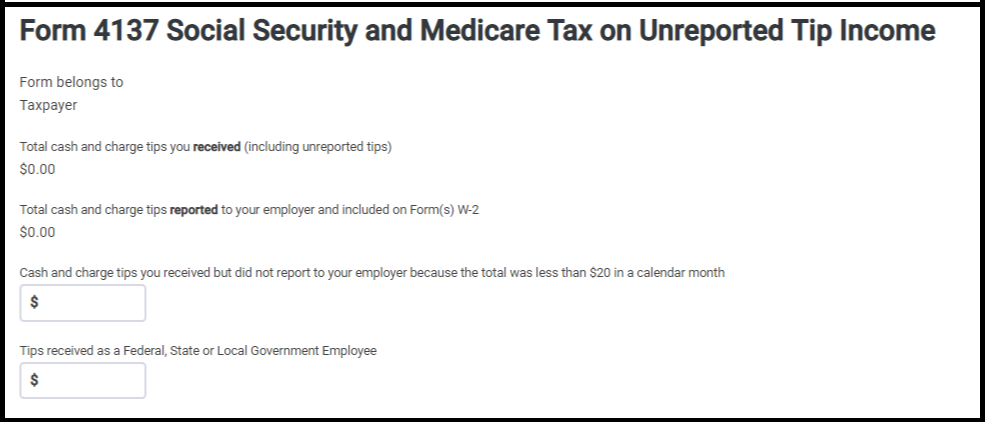

Tax on Unreported Tip Income - Form 4137

Form 4137 is used to calculate the social security and Medicare tax owed on tips the taxpayer did not report to his or her employer, including any allocated tips shown on Form W-2 (box 8) that the taxpayer must report as income. The taxpayer must file Form 4137 if he or she received cash and charge tips of $20 or more in a calendar month and did not report all those tips to the employer.

Tax on Early Distribution - Form 5329

Any payment that the taxpayer receives from an IRA or qualified retirement plan before reaching age 59½ is normally called an “early” or “premature” distribution. If the taxpayer includes amounts from a Form 1099-R (IRA and Pension Distributions) on the tax return, he or she may be subject to a 10% penalty if the funds have been withdrawn from the retirement plan before the taxpayer has reached age 59 ½.

In addition to paying regular income tax on that money (it's taxed along with the rest of the income), the taxpayer will have to pay a penalty for the "early" distribution.

Distributions from the following types of retirement plans are subject to this 10% penalty:

- A qualified retirement plan (like a 401(k) or a Keogh plan)

- A traditional IRA

- A Roth IRA

- An annuity (tax-deferred)

- A modified endowment contracts

Household Employment Tax - Schedule H

If the taxpayer is required to pay employment taxes on domestic help, the tax program will calculate them along with the regular income tax on Form 1040. However, you will need to complete Schedule H, Household Employment Taxes, and include it with the tax return.

First-time Homebuyer Repayment - 5405

If a taxpayer is required to repay the First-Time Homebuyer Credit you must file Form 5405. For more information on who must repay the credit, see the instructions for Form 5405.

Tax for Children Under Age 18 - Form 8615

If a child under age 18 had more than $2,100 in unearned income, compute the child's tax using Form 8615, Tax for Certain Children Who Have Earned

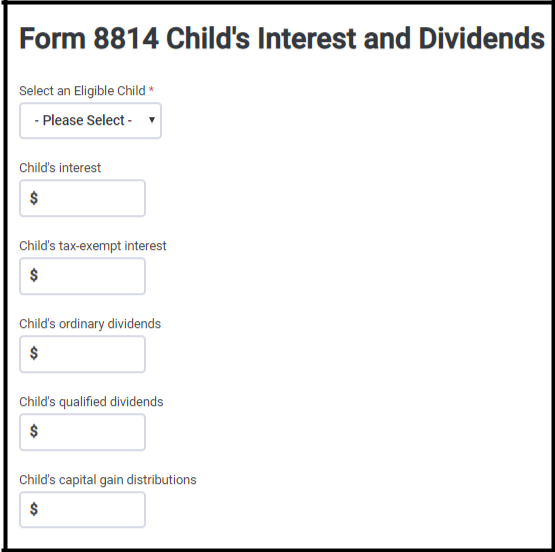

Income Child’s Interest/Dividend Earnings - Form 8814

If your taxpayer’s child's income was in the form of interest, dividends, and capital gain distributions (e.g., from mutual funds), and the child’s AGI was less than $10,500, law allows them to elect to report the income on the taxpayer's own return rather than filing a separate return for the child.

The IRS allows preparers to treat the child's income as the taxpayers. For a child under 18, all unearned income above $2,100 must be taxed based on the tax tables listed in the instructions.

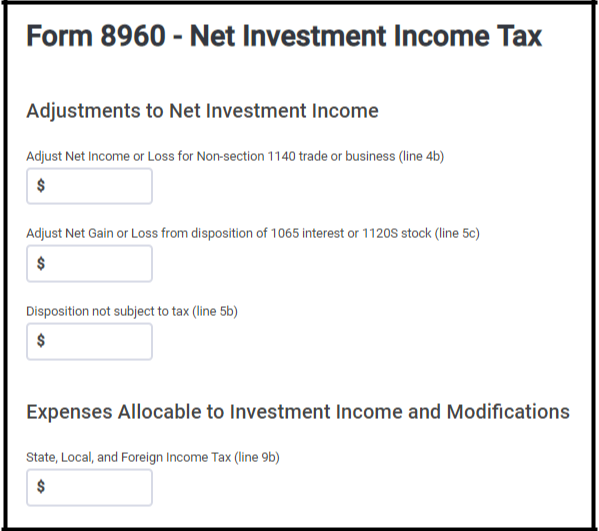

Net Investment Income Tax—8960

From 8960 to figures the amount of your Net Investment Income Tax (NIIT).

Generally, net investment income includes gross income from interest, dividends, annuities, royalties, and rents, unless they are derived from the ordinary course of a trade or business that is not:

- A passive activity; or

- A trade or business of trading in financial instruments or commodities.

In addition, net investment income includes other gross income derived from a trade or business that is:

- A passive activity; or

- A trade or business of trading in financial instruments or commodities.

Additionally, net investment income includes net gain (to the extent considered in computing taxable income) attributable to the disposition of property other than property held in a trade or business that is not:

- A passive activity or

- A trade or business of trading in financial instruments or commodities.

To arrive at net investment income, the above items are reduced by educations allowed against the income tax which are properly allocable to those items of gross income or net gain.