Deductions

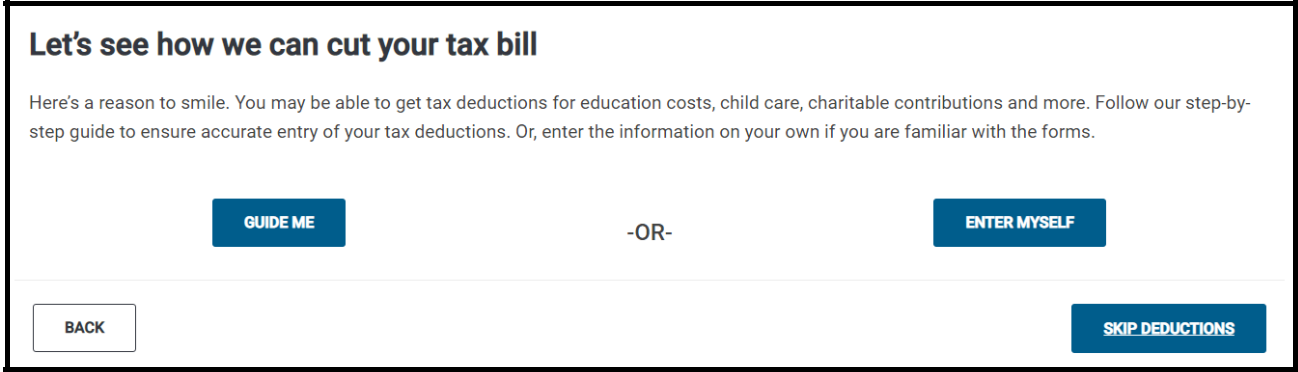

The Deductions portion of the Federal Section is used to enter all deductions, adjustments or subtractions on the tax return. The Preparer will be given two options from the main income page.

Select Guide Me to launch a step-by-step series of questions to help determine the various types of deductions that should be entered on the tax return. To enter deductions without assistance, select Enter Myself. This will open the deductions entry screen which lists the various types of deductions that should be reported on the tax return. Select a Begin or an Edit button to enter/edit a deduction.

Standard Deduction

The Standard Deduction is automatically calculated based on the taxpayer’s filing status and compared to the itemized deductions. The deduction that benefits the taxpayer most will be used on the tax return.

Itemized Deduction

In lieu of the Standard Deduction, the IRS allows deductions for certain expenditures. These Itemized deductions include expenditures such as mortgage interest, property taxes, etc. which are deductible on Schedule A, allowing a taxpayer to reduce their Adjusted Gross Income (AGI) on their tax return.

NOTE: Under the Tax Cuts and Jobs Act, Itemized Deductions have changed significantly. This section will reflect the current tax law.

In the Itemized Deductions section, the preparer will be able to enter:

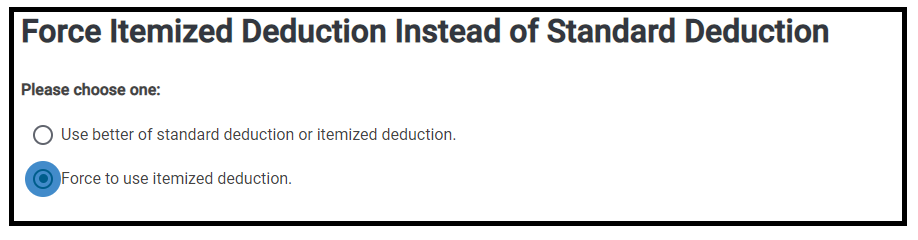

Use Standard or Itemized Deduction

The preparer can force the Web1040 Pro program to elect itemized deductions only, disregarding the Standard Deduction, using this option.

NOTE: The program will automatically choose the more beneficial deduction for the taxpayer. However, if the preparer would like to force the standard deduction simply delete all itemized deduction entries.

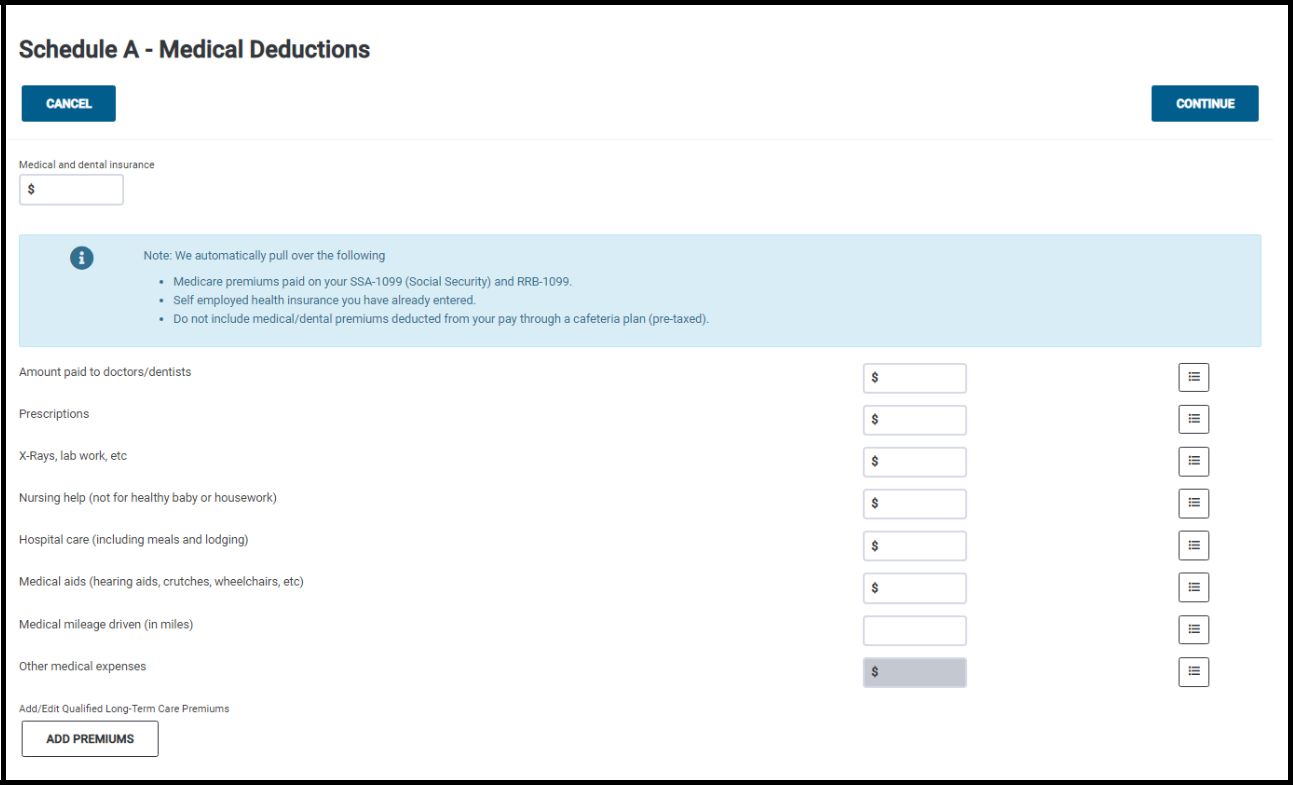

Medical and Dental Expenses

These are the taxpayer’s reasonable and necessary unreimbursed expenses relating to health care for the taxpayer, spouse (if filing jointly) and their dependents. This includes, but is not limited to, expenses for the following:

- Doctors

- Dentists

- Hospitals

- Transportation to medical care

- Prescriptions, and

- Health insurance premiums

If either the taxpayer or the spouse was born before January 2, 1953, they can deduct the portion of his or her medical expenses with itemized deductions that exceeds 10 percent of the taxpayer's adjusted gross income (AGI).

If they were born after, they can deduct the expenses exceeding 10 percent of their adjusted gross income (AGI).

Taxes You Paid

Additional State and Local Income Tax

Income taxes that the taxpayer paid to the state are deductible up to $10,000. The tax program will automatically pull the state withholdings from the taxpayer’s W-2s to the Schedule A. Rather than use the income taxes paid to the state, the taxpayer can elect to deduct state and local general sales taxes. The software will calculate whether the state and local income tax withheld is greater than the state and local sales taxes and use the greater amount for the deduction.

Sales Tax Worksheet

Enter the State, number of days lived in the state, local sales tax percentage, and State sales tax percentage. Once done, enter the total general sales taxes paid on large purchases ONLY. The program will automatically use the IRS general sales tax calculation based on previous information to calculate the client’s general deduction.

Real Estate Taxes

Any tax the taxpayer paid for real estate property is deductible. The tax is deductible on ALL real estate property that is owned, and that the taxpayer paid the tax on during the current tax year.

Personal Property Taxes

Enter personal property tax paid by the taxpayer, but only if it is based on value alone, and it is charged on a yearly basis (for example, ad valorem tax on car tags).

NOTE: The combined deduction limit for all of these taxes paid is $10,000.

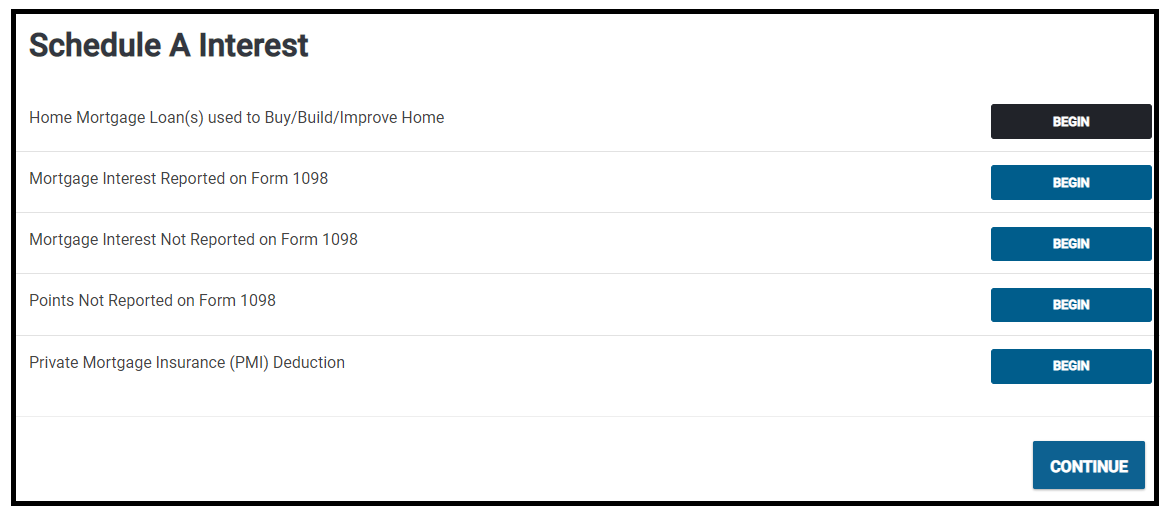

Mortgage Interest and Expenses

Interest paid on mortgages of the taxpayer’s primary home may be reported here. This is a straight deduction without a minimum amount to meet.

The taxpayer can deduct home mortgage interest if all the following conditions are met:

- The taxpayer must itemize deductions on Schedule A

- The mortgage must be a secured debt on a qualified home and the taxpayer has an ownership interest (See IRS Publication 936).

The interest that the taxpayer paid will be reported on Form 1098.

Under the TCJA, Home Equity Interest is no longer deductible. However, interest on loans taken out with the purpose to buy, build or improve your home can still be deducted. For loans within this category, you will report them under Mortgage Interest Deductions on the Schedule A under the first option listed:

Points are an upfront or prepaid interest charge on a mortgage. These points are deductible in full in the year that they are incurred if the mortgage is used solely for the house and not any other item.

Primary Mortgage Insurance (PMI) Premiums have been eliminated under the TCJA as of December 31, 2017.

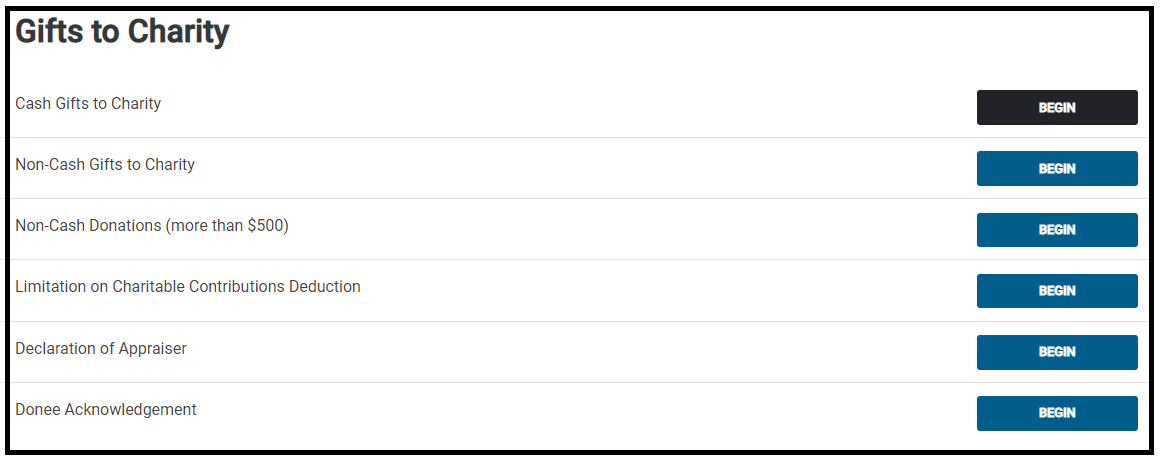

Gifts to Charity – Form 8283

Charitable Contributions are recorded in Itemized Deductions using this menu option.

Form 8283 – Noncash Charitable Contributions (to be used if the total deduction is over $500) is accessed from this menu. Under the new tax law, cash contributions are limited to 60% of the taxpayer’s AGI.

If the taxpayer made total noncash gifts over $500 for the year, the tax preparer should complete and attach to the tax return IRS Form 8283. If any single gift or group of similar gifts was valued at over $5,000, an appraisal of the item from a qualified appraiser is required.

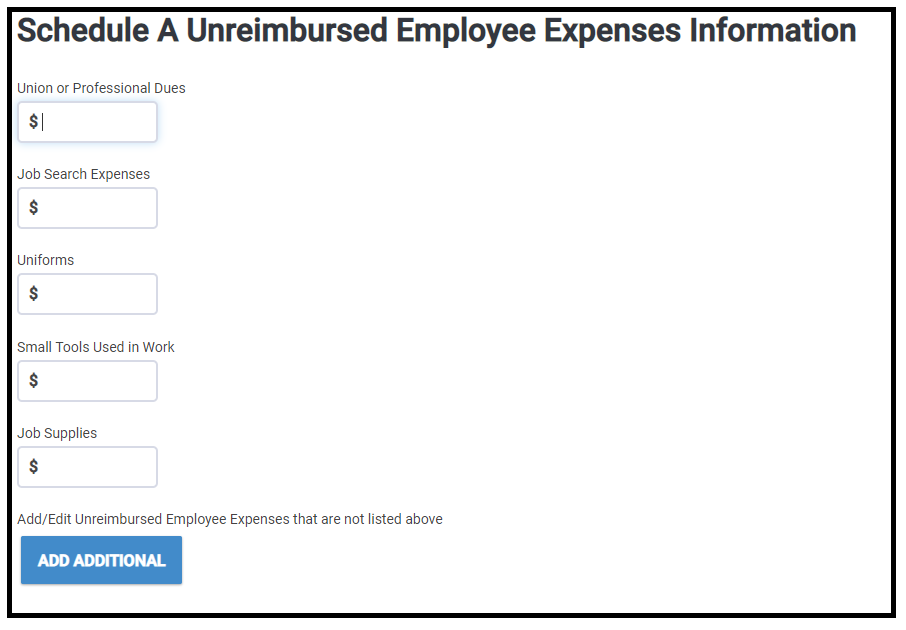

Unreimbursed Employee Business Expense

Under the new tax law, all Unreimbursed Employee Expense Deductions have been eliminated unless you are employed in one of the following jobs:

- Armed Forces reservist, including Army, Navy, Marine Corps, Air Force, Coast Guard, Army National Guard, and the Reserve Corps of the Public Health Service

- Qualified performing artist

- Fee-basis local and/or state government official

- Eligible Educator

Those with these occupations will not take a deduction, but rather an adjustment for their expenses.

See Form 2106 for instructions.

Examples of job-specific expenses:

- Safety equipment, small tools, and supplies needed for the taxpayer’s job.

- Uniforms required by the employer that are not suitable for ordinary wear.

- Protective clothing required for work, such as hard hats, safety shoes, and glasses.

- Physical examinations required by the employer.

- Passport for a business trip.

- Job search expenses in the taxpayer’s present occupation.

- Depreciation on a computer your employer requires the taxpayer to use in their work.

- Dues to professional organizations and chambers of commerce.

- Licenses and regulatory fees.

- Subscriptions to professional journals.

- Occupational taxes.

- Union dues and expenses.

- Fees to employment agencies and other costs to look for a new job in the taxpayer’s present occupation, even if you do not get a new job.

- Certain work-related educational expenses.

- For a complete list of expenses, see IRS Publication 529.

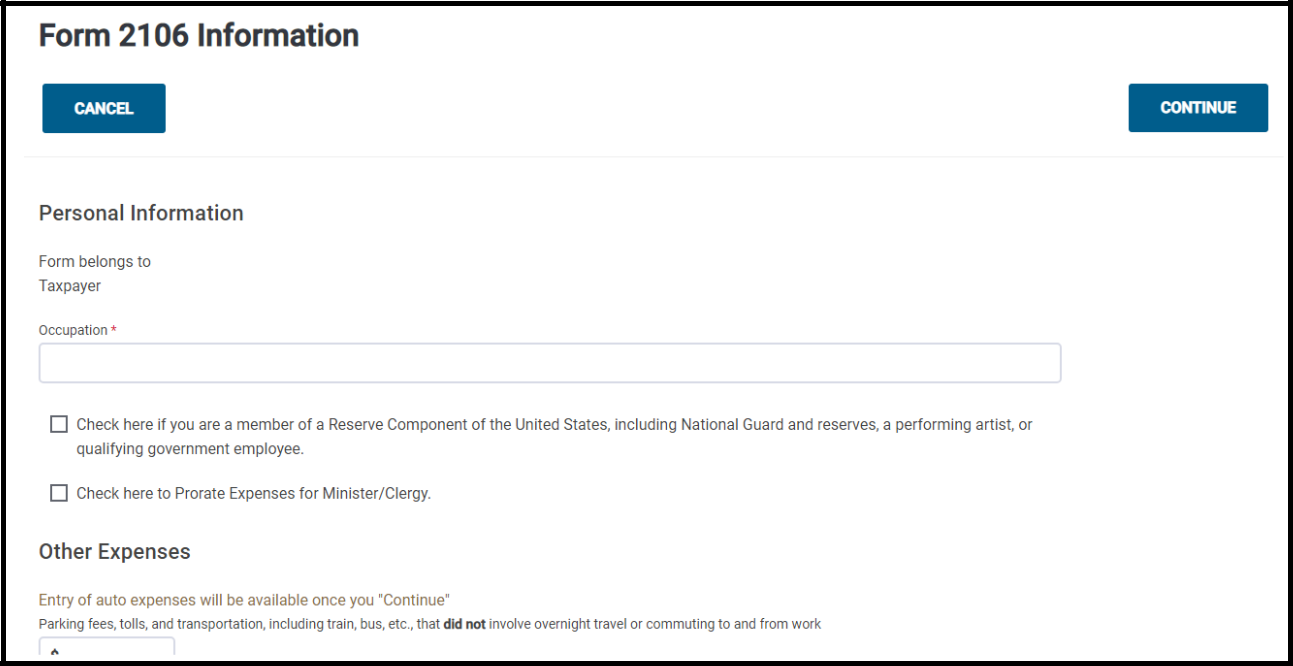

Job-Related Travel Expenses (Form 2106)

Travel expenses are expenses that were paid in relation to transportation or travel for business. Under the new tax law, these expenses can only be deducted for member of the Armed Forces, qualifying performing artists, and the other jobs that also qualify for the Unreimbursed Employee Expenses deduction.

For a travel expense to qualify for a deduction, the travel must have been primarily in relation to the taxpayer’s job.

Qualifying travel expenses include:

- Parking fees

- Tolls

- Transportation (such as taxis and shuttles)

- Lodging

- Airplane travel

- Car rental for business purposes, and

- Expenses for the business use of your personal vehicle (such as mileage).

Any meals and entertainment expenses incurred for business purposes would also be considered a travel expense.

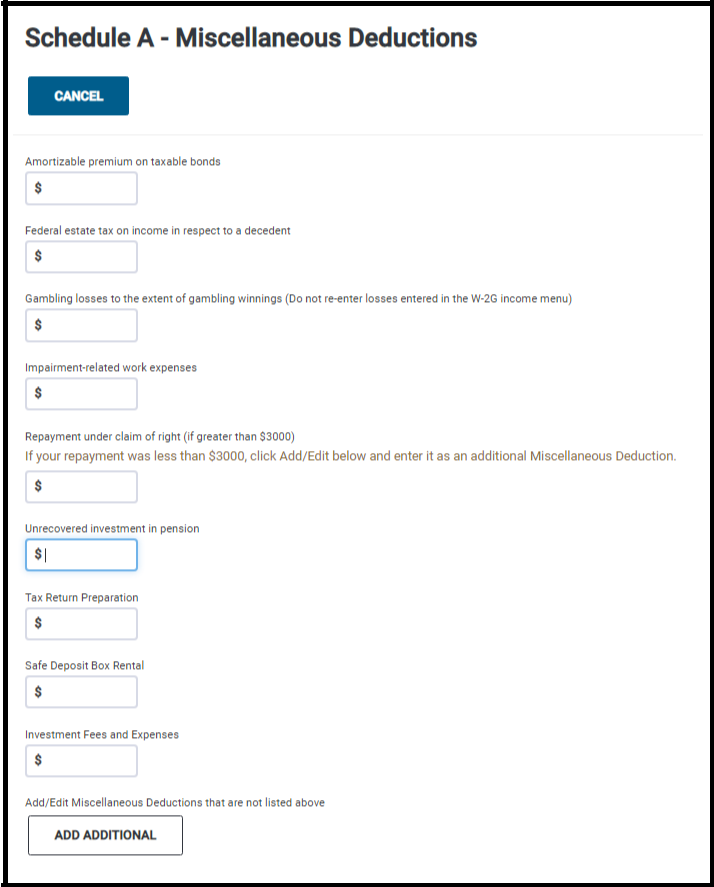

Miscellaneous Deductions

Deductions Not Subject to the 2% Limit include but are not limited to:

- Amortizable Premiums on Taxable Bonds

- Federal estate tax on income in respect to a decedent

- Gambling losses up to the amount of gambling winnings incurred in the tax year

- Impairment related to work expenses if the taxpayer has a physical or mental disability that limits their employment or major life activities

- If the taxpayer had to repay more than $3,000 of income that was included in their income for an earlier year (this is known as a "claim of right.")

- Unrecovered investment in a Pension

- Tax Return Preparation fees

- Investment Fees and Expenses

NOTE: Under the TCJA, these deductions have been eliminated. If you have a state that still allows the taxpayer to report any of these deductions, you may enter these for those purposes only. These deductions will not calculate with the other Itemized Deductions for the Federal Deduction amount.

Less Common Deductions

Casualties and Losses – If the taxpayer suffered the results of a theft, accident, fire, flood, or other casualty or loss during the year in a federally declared disaster area, he or she may be able to deduct some of the unreimbursed losses.

Business Use of Home – Deductible expenses for business use of the taxpayer’s home include the business-related portion of:

- Real estate taxes

- Mortgage interest

- Rent

- Casualty losses

- Utilities

- Insurance

- Depreciation

- Maintenance, and

- Repairs

Taxpayers may not deduct expenses for lawn care in general or for painting a room not used for business. Taxpayers can elect to take this deduction on you Schedule C or Itemized Deductions but cannot claim the expense in both places.

Investment Interest – Investment interest is interest that was paid on money that was borrowed to buy property that is held for investment. If the taxpayer paid this type of interest, they may be eligible for a deduction.

Examples of this type of interest include:

- Interest that was paid on securities in a margin account

- Interest that was paid on a loan that the taxpayer took out to invest in a business with someone else, and

- Interest that was paid on a loan that the taxpayer used to buy stocks.